The better your credit score the better your opportunity is to successfully acquire a home loan from the major banks!

Your credit score is based on your credit behaviour which includes if you pay your accounts on time, how much debt you have (exposure) and how it compares to other consumers.

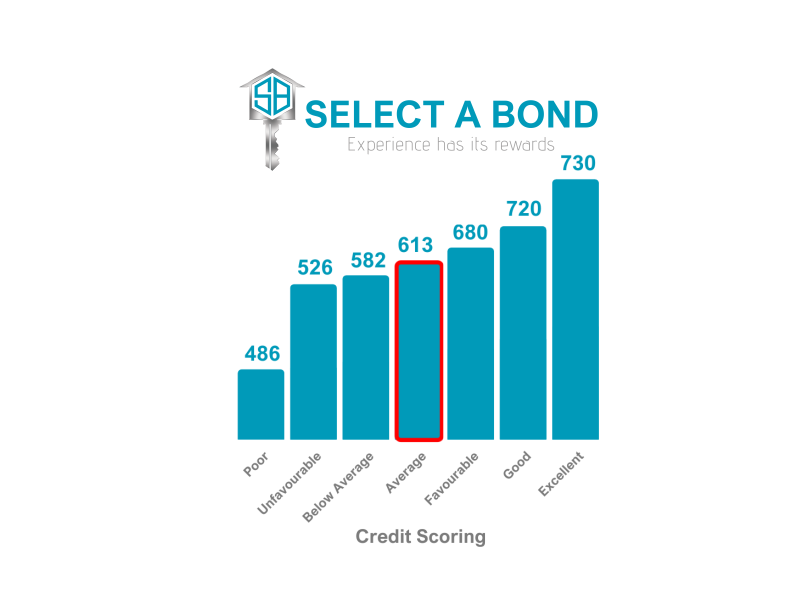

Although it is possible to acquire a home loan with an average score, it is recommended that if you are able to improve your score, the higher the score the better offers you will receive. To improve your credit score you can make the following changes to your finances and budgets:

1) Regularly keep a careful watch on your credit score and action all issues that arise – ensure that all paid-off debt is no longer on your record or at nil balance and the account is closed.

2) Appearance of existing or historical credit, (i.e. credit cards, cell phone accounts, retail credit etc) should indicate that you have managed effectively and without defaulting on any of the payments. If not, you need to get them under control by clearing the debit and paying regularly.

3)If you do owe several different debtors then consider consolidating your debt or you can reduce your overall debt by paying more than your instalment on each account and clearing the smaller debts first.

4) Never pay less than the minimum instalment for all of your accounts and ensure that you always pay on time. Set up scheduled payments for all store accounts to avoid overlooking monthly instalments.

5) Monitor how much credit you have available to you and avoid using more than 35% (i.e. if you have a credit card with a limit of R2 000, try to maintain the amount owing balance at under R700). Never max out your credit cards and do not borrow more than you need!

6) Securing an additional income stream always helps, but avoid unstable or irregular income and frequent changes in your address – a stable credit history is key!

7) It is good practice to have cleared your debt before applying for more and never open too many accounts at the same time.

8) If married with a marriage agreement in place (Ante-Nuptial Contract) and your spouse is to be included on a bond application, or if married in Community of Property then you must ensure that your partner manages their credit score in the same manner.

9) When your bond has been approved never engage with any further credit agreement until after the registration has taken place, (i.e. motor vehicle, expensive furniture or appliances).

10) Avoid continual monthly loans as salary top-ups, this is strongly frowned upon and may damage your apparent financial status.

11) If you are under debt review, no bank can extend further credit until this is removed from your credit record, you must have a Clearance Certificate and generally be prepared to wait 6-12 months to create an acceptable credit history before applying for a home loan.

Contact us today for a FREE prequalification assessment, indicating a home loan amount for which you may qualify.

Martin 082 447 3463

Kim 079 835 1476