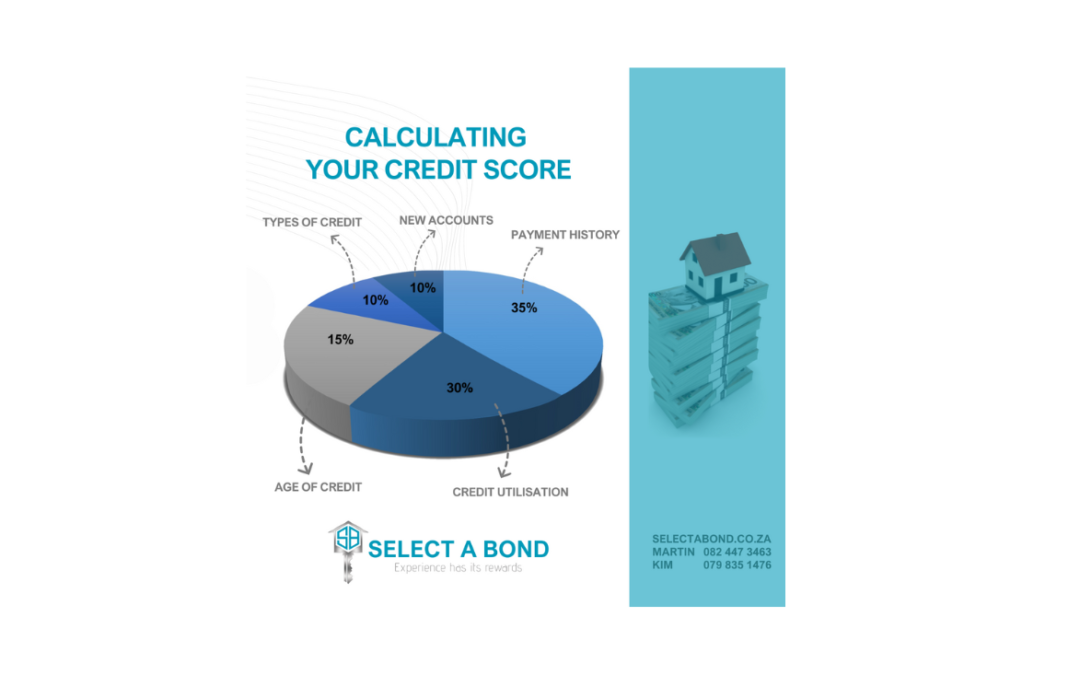

When determining the value of your home loan the banks will look at your credit score. This credit score is determined by the following factors:

Types of credit 10%

It is always good to have different types of credit in your name (credit cards, cell phone accounts, retail credit, ext.) and they will look at the difference between good debt (car/assets) and the not so favoured debt (unsecured – credit cards, personal loans).

New Accounts 10%

This looks at how many accounts you have in your name and how often you have applied for credit. It is good practice to have cleared your debt before applying for more, and never open too many accounts at the same time. Do not overkill with checking of your report, as changes are generally monthly.

Payment history 35%

Paying your accounts every month with the full instalment (or more) and on time is key to securing a home loan. Late payments are frowned upon – remove the human error factor by creating debit orders or scheduled payments.

Age of credit 15%

The age of your credit is determined by how long you have had your accounts (old and new) and then they calculate the average age of all of your accounts.

Credit utilisation 30%

This looks at how much credit you have available and how you have managed that credit. Ideally, you don’t want to use more than 35% of your available credit and never max out your credit cards.

To determine how much of a home loan you qualify for, please contact

Martin 082 447 3463

Kim 079 835 1476